Var value at risk

Value at risk ( VaR ) is a statistical technique used to measure and quantify the level of financial risk within a firm or investment portfolio over a specific time frame. This metric is most commonly used by investment and commercial banks to determine the extent and occurrence ratio of potential losses in their institutional . A: Value at risk ( VaR ) is one of the most widely known measurements in the process of risk management. Topically, VaR accomplishes all . The VaR of a portfolio is the worst loss expected to be suffered over a given period of time with a given probability.

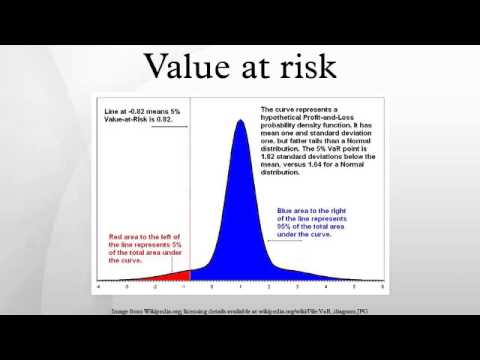

The time period is known as the holding perio and the probability is known as the confidence interval.

VaR is not an estimate of the worst possible loss, but the largest likely loss. What is the most I can lose on this investment? This is a question that almost every investor who has invested or is considering investing in a risky asset asks at some point in time. Value at Risk tries to provide an answer, at least within a reasonable bound. A risk management model that calculates the largest possible loss that an institution or other investor could incur on a portfolio.

Value at risk describes the probability of losing more than a given amount of assets, based on a current portfolio. It was developed (not originated) at JPMorgan in response to a demand from then . VAR is important because it is used to allocate capital to market risk for banks, under their Risk.

Based Capital requirements. This is illustrated in Exhibit for a VaR metric. VAR is a measure of market risk, and is equal to. VAR ) – An approach to risk used in banking and investment, but less often by insurers and reinsurers.

The value at risk ( VaR ) measures the risk of loss associated to financial assets. Abstract: A large part of general microeconomic (in insurance) theory has been concerned with devising robust and analytically sound techniques for assessing the risk in insurance premium calculation. We need to address a simple actuarial.

Value-at-risk ( VaR ) is a Probabilistic Metric of Market Risk (PMMR) used by banks and other organizations to monitor risk in their trading portfolios. For a given probability and a given time horizon, value-at-risk indicates an amount of money such that there is that probability of the portfolio not losing more than that amount of . Value At Risk is a widely used risk management tool, popular especially with banks and big financial institutions. There are valid reasons for its popularity – using VAR has several advantages. But for using Value At Risk for effective risk management without unwillingly encouraging a future financial disaster, it is crucial to . Lecture 7: Value At Risk ( VAR ) Models.

Developed for educational use at MIT and for publication through MIT OpenCourseware. No investment decisions should be made in reliance on this material.